Personal Loans in 2026: How to Navigate the Landscape When Your Credit Isn’t Perfect

The year 2026 has brought a fresh wave of lenders eager to fill gaps left by traditional banks, especially for borrowers with credit scores below 670. While many institutions still prefer higher FICO scores, several online lenders now offer fixed‑rate installment loans that cater to those who need quick cash for emergencies, debt consolidation, or large purchases. In this deep dive, we’ll examine the current market, highlight key players, and provide practical tips on how to choose the right loan without falling into common pitfalls.

Why Fixed‑Rate Installment Loans Matter Now

Fixed‑rate installment loans—often called personal loans—provide a predictable payment schedule. Unlike credit cards or payday lenders, the interest rate stays constant for the life of the loan, meaning your monthly payment won’t surprise you when market rates shift. For many borrowers with moderate credit, this stability is a major advantage.

In 2026, the average APR on personal loans ranges from about 7% to 36%, depending largely on credit history and the lender’s underwriting criteria. The term typically spans two to seven years, offering flexibility for those who want to balance monthly affordability against total interest paid.

According to a recent NerdWallet guide, the typical loan amount sits between $1,000 and $50,000, though some platforms now extend up to $100,000 for borrowers with solid financial profiles.

How Lenders Evaluate Applicants

- Credit Score: Most lenders require a minimum FICO score of 580–620. However, a handful accept scores as low as 550, albeit at higher interest rates.

- Debt‑to‑Income Ratio (DTI): A lower DTI increases the likelihood of approval and can secure more favorable terms.

- Employment & Income History: Steady employment or a consistent income stream reassures lenders that you can repay on time.

- Other Credit Lines: Existing mortgages, auto loans, or credit cards can affect the lender’s risk assessment.

Top Personal Loan Lenders for Scores Below 670

While many borrowers are familiar with Avant and OneMain Financial, a few newer entrants have carved out niches by offering competitive rates to those with fair credit. These lenders blend technology‑driven underwriting with personalized service.

| Lender | Minimum Credit Score | Loan Amount Range | Typical APR | Key Feature |

|---|---|---|---|---|

| Avant | 580 | $3,000 – $35,000 | 7%–36% | Fast approval; funding the next day if approved by 5:30 PM ET. |

| OneMain Financial | 600 | $3,000 – $40,000 | 9%–32% | Flexible terms of 24–60 months. |

| Upgrade | 650 | $5,000 – $35,000 | 7%–30% | Credit‑building option with a “Payback” feature. |

| LightStream (a SunTrust brand) | 660 | $5,000 – $50,000 | 6%–25% | Low rates for borrowers with strong credit. |

Each lender’s algorithm weighs factors differently. For example, Avant uses a mix of credit bureau data and alternative metrics, while LightStream relies heavily on traditional credit scores. Understanding these nuances can help you target the best fit for your financial profile.

Why “Fast Funding” Is Not Always Fast Money

A common lure in personal loan marketing is the promise of instant approval and same‑day disbursement. However, even when a lender processes your application quickly, hidden fees or high APRs can erode any perceived benefit. It’s essential to compare the full terms and conditions before committing.

In many cases, a well‑structured loan with a slightly longer approval time may offer lower overall costs. Always read the fine print—especially regarding prepayment penalties or origination fees that can add up over time.

The Role of Soft vs. Hard Credit Inquiries

When you apply for a personal loan, the lender performs a credit inquiry. A hard pull can temporarily lower your score by a few points. In contrast, a soft pull (e.g., when you check your own credit) has no impact.

Lenders typically conduct hard inquiries to assess risk accurately. However, some platforms allow multiple applications with only one hard pull per 30‑day period—an advantage for shoppers comparing rates.

Managing Your Credit Score During the Application Process

- Limit Applications: Each hard inquiry can cost up to 5 points. Space out applications over at least a month.

- Check Your Credit Early: A soft pull lets you review your score before applying, ensuring you’re ready for the next step.

- Monitor Changes: Use free tools from Credit Karma or NerdWallet to watch how inquiries affect your credit.

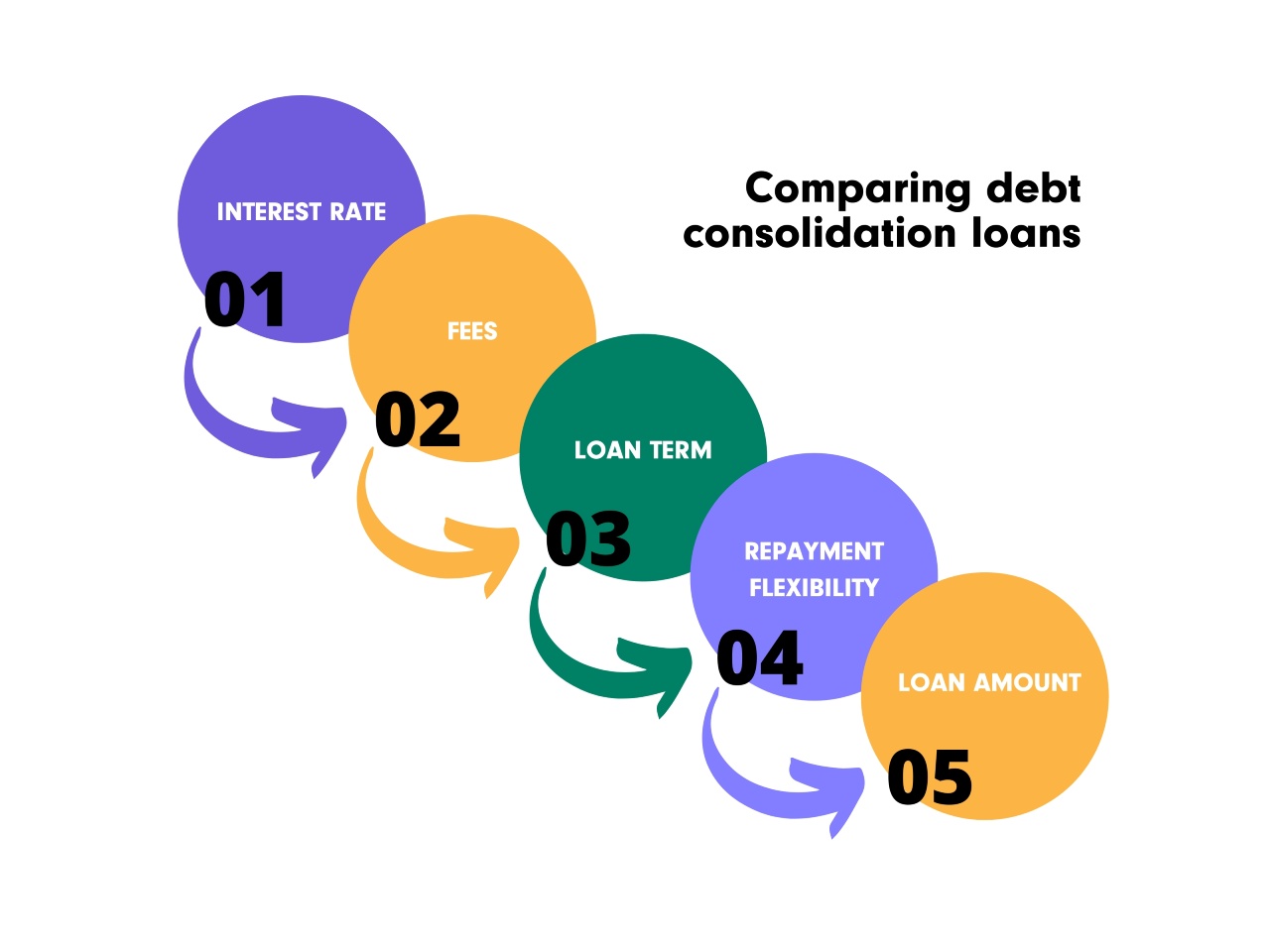

Debt Consolidation: The Sweet Spot of Personal Loans

Many borrowers turn to personal loans as a way to consolidate high‑interest credit card debt. By combining multiple balances into one fixed‑rate payment, you can reduce monthly interest and streamline finances.

The Happy Money Study found that only 8% of respondents had consolidated or refinanced debt, highlighting a missed opportunity for savings.

A typical consolidation loan may offer an APR between 10% and 18%, significantly lower than credit card rates. When properly managed, this can shave years off your payoff timeline and free up cash flow for other priorities.

Choosing the Right Consolidation Plan

- Calculate Total Interest: Compare the cumulative interest paid over the loan term versus current card balances.

- Check for Prepayment Penalties: Some lenders charge fees if you pay off the loan early.

- Consider a Co‑Signer: If your score is borderline, a co‑signer can secure lower rates.

How to Apply for a Personal Loan in 2026

The application process has become almost entirely digital. Most lenders offer instant decision tools that evaluate your credit profile and provide an initial rate quote within minutes.

“I was able to get my loan approved in less than five minutes,” says Maria Lopez, a recent borrower who secured a $12,000 consolidation loan from Avant. “The online form was straightforward, and I received the funds the next day.”

Here’s a step‑by‑step guide:

- Gather Documents: Pay stubs, tax returns, bank statements, and proof of employment.

- Check Your Credit Score: Use a free tool to ensure you meet the lender’s minimum requirements.

- Compare Lenders: Look at APRs, terms, fees, and customer reviews. A quick comparison table can save hours.

- Apply Online: Fill out the application form; many lenders now offer “no‑credit‑check” pre‑qualification.

- Review the Loan Agreement: Pay close attention to origination fees, late payment penalties, and prepayment terms.

- Receive Funds: Most loans deposit directly into your bank account within one business day.

Post‑Approval Tips

- Set Up Auto‑Pay: Avoid missed payments and potentially lower your rate.

- Track Your Progress: Use an online calculator or spreadsheet to monitor how much interest you’re saving over time.

- Reevaluate After a Year: If your credit improves, consider refinancing for better terms.

Why Jet Loans Is Worth Considering in 2026

As personal loan options continue to diversify, Jet Loans has emerged as a strong contender for borrowers seeking transparent terms and flexible repayment plans. The platform’s algorithm blends traditional credit data with alternative metrics—such as utility payment history—to broaden eligibility without compromising on risk.

Clients report an average approval time of under 48 hours, with funding typically available within one business day after approval. Moreover, Jet Loans offers a unique “Pay‑Later” feature that allows borrowers to delay the first payment for up to 30 days, providing breathing room during financial transitions.

With competitive APRs ranging from 8% to 28%, depending on credit profile, and no prepayment penalties, Jet Loans stands out as a modern solution for debt consolidation, emergency cash needs, or sizable purchases that exceed the limits of credit cards.

Real‑World Impact

A recent case study highlighted how a small business owner used Jet Loans to refinance two high‑interest lines of credit. The new loan’s 12% APR saved the company over $4,000 in interest annually and allowed them to redirect funds toward marketing initiatives.

Another user, a single parent with a FICO score of 610, found that Jet Loans’ flexible payment schedule helped her avoid late fees on her car loan while consolidating credit card debt. “I finally feel like I’m in control again,” she shared.

Key Takeaways for 2026 Borrowers

- Fixed‑rate installment loans offer predictable payments and can be a safer alternative to revolving credit.

- Many lenders now accept scores as low as 550, but higher rates apply; shop around before committing.

- Soft pulls keep your score intact while you explore options; hard inquiries should be spaced out.

- Debt consolidation can dramatically reduce interest and simplify finances if managed wisely.

- Platforms like Jet Loans provide transparency, quick funding, and flexible terms—making them a compelling choice for borrowers with moderate credit.

By understanding the current landscape, comparing offers carefully, and leveraging technology‑driven lenders, you can secure a personal loan that aligns with your financial goals without compromising long‑term stability.

Recent Comments